A statutory requirement outlining the financial estimates to deliver the Corporate Business Plan

Expenditure that extends the capacity of an existing asset to provide benefits to new users at the same standard as is provided to existing beneficiaries.

Expenditure on an existing asset or on replacing an existing asset that returns the service capability of the asset to original capability.

Expenditure which enhances an existing asset to provide a higher level of service or expenditure that will increase the life of the asset beyond its original life.

Financial Assets include cash, investments, loans to community groups, receivables and prepayments, but excludes equity held in Council businesses, inventories and land held for resale.

Financial Sustainability is where planned long-term service and infrastructure levels and standards are met without unplanned and disruptive increases in rates or cuts to services.

Net Lending/ (Borrowing) equals Operating Surplus / (Deficit), less net outlays on non-financial assets. This result is a measure of the Council’s overall (i.e. Operating and Capital) budget on an accrual basis. Achieving a zero result in any one year essentially means that the Council has met all of its expenditure (both operating and capital) from the current year’s revenues.

Non-financial or Physical Assets refers to infrastructure, land, buildings, plant, equipment, furniture and fittings, library books and inventories.

Operating Deficit is where operating revenues are less than operating expenses (i.e. operating revenue is therefore not sufficient to cover all operating expenses).

Operating Expenses are operating expenses shown in the Income Statement, including depreciation, but excluding losses on disposal or revaluation of non-financial assets.

Operating Revenues are incomes shown in the Income Statement but exclude profit on disposal of non–financial assets and amounts received specifically for new/upgraded assets (e.g. from a developer).

Operating Surplus is where operating revenues are greater than operating expenses (i.e. operating revenue is therefore sufficient to cover all operating expenses) but does not take into account any capital expenditure.

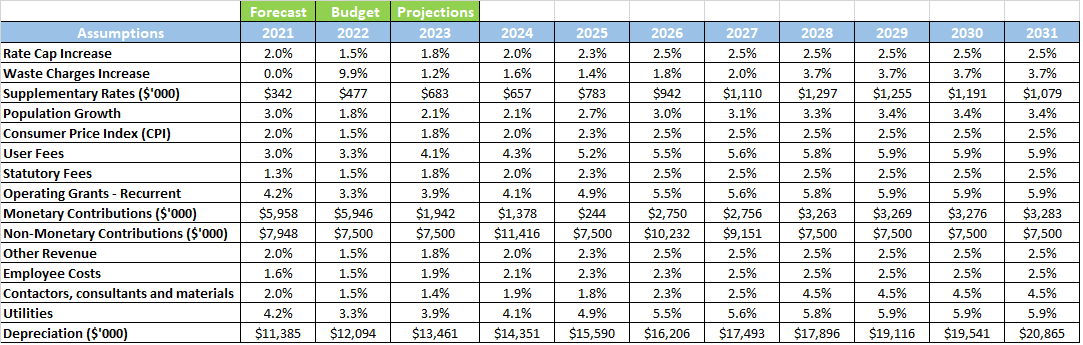

The maximum annual rate of increase that councils can apply to their rates revenue.

Cash and cash equivalents that are not available for use other than a purpose for which it is restricted and includes cash to be used to fund capital works expenditure from the previous financial year.

The statement of capital works shows the expected internal and external funding for capital works expenditure and the total proposed capital works expenditure for the forthcoming year with a comparison with forecast actual.

Means a statement which shows all Council staff expenditure and the number of full-time equivalent Council staff.

Unrestricted cash represents all cash and cash equivalents other than restricted cash.

.png)

.png)